Business

Riot Platforms stock explodes 115 percent in 90 days but here’s why analysts are still cautious about its future

Bitcoin production is booming and Riot’s stock price just soared — but index removals, projected losses, and over-reliance on crypto are raising fresh red flags among experts.

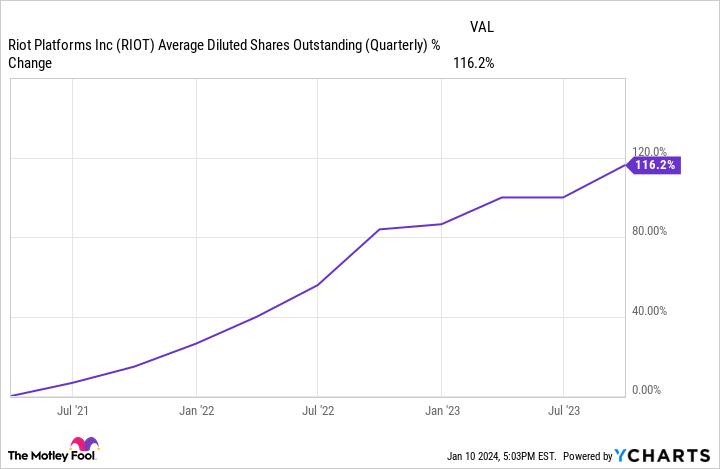

Riot Platforms, Inc. — one of the leading players in the Bitcoin mining industry — has seen its stock price surge by a staggering 115% over the last quarter, driven by increased production output and rising investor optimism. But behind this bullish breakout lies a complicated story of growth, volatility, and financial caution that experts say should not be ignored.

Table of Contents

As per a recent update by Simply Wall St, Riot Platforms (NASDAQ: RIOT) mined 450 Bitcoins in June 2025, a significant rise compared to 255 Bitcoins mined during the same period last year. This milestone is a direct result of Riot’s strategic investments in its Corsicana and Rockdale facilities, where it has ramped up its hash rate capacity to strengthen its mining output.

But while operational performance looks bright, the removal of Riot from multiple Russell indices by the end of June has cast a shadow over its market credibility. Index exclusions often signal concern from institutional players and can limit access to passive inflows from funds that track such benchmarks.

“Despite significant gains in operations, the broader market still reacts to index placements and institutional sentiment,” said analysts reviewing Riot’s outlook. “There’s a gap between fundamentals and perception.”

Long-Term Growth vs Short-Term Risks

Over a five-year period, Riot Platforms has delivered a total return of 524.32%, a remarkable performance considering the volatile nature of Bitcoin and broader tech sectors. However, the company’s current valuation — at $13.86 per share, roughly 17.36% below the average analyst target of $16.27 — suggests that the stock might still be undervalued by Wall Street standards.

Yet, that doesn’t make it risk-free.

Despite its soaring production numbers, Riot is still not profitable. Its Earnings Per Share (EPS) continues to reflect a loss, and the company’s roadmap toward profitability remains uncertain. Analysts project a 20% revenue growth, but many note that high capital expenditures, ongoing infrastructure expansion, and Bitcoin’s price volatility could weigh down Riot’s financial future.

“We’re looking at a business that’s investing heavily in its future — but it’s a future that depends largely on the price of Bitcoin,” said a senior researcher at Morningstar.

A Broader Strategy: Mining Meets AI

Riot is not just banking on Bitcoin. It’s actively exploring opportunities in the AI and High-Performance Computing (HPC) space. With the AI boom accelerating, Riot’s pivot could open up new revenue streams, particularly in compute-intensive operations. This diversification move may protect Riot from the cyclical nature of cryptocurrency markets.

Still, the company will need time, money, and regulatory clarity to execute this vision effectively.

Market Dynamics at Play

The broader NASDAQ market has remained largely flat in the past week, and Riot’s outperformance stands in stark contrast. This suggests that the stock’s movement is being driven more by sector-specific news and retail interest than broad-based institutional inflows.

Notably, the company’s removal from key indices like the Russell 2000 may continue to act as a psychological barrier for big fund managers who depend on index tracking for allocations.

And then there’s Bitcoin itself — currently hovering around $65,000 — which has recently shown signs of resistance. If the crypto market dips, Riot’s fortunes may follow suit, regardless of its internal achievements.

What Investors Should Watch

- Bitcoin Price Trends: Any major fluctuation in BTC price directly impacts Riot’s bottom line.

- Hash Rate Expansion: Riot’s success hinges on its ability to keep scaling up mining capacity.

- AI Integration: Progress in this area could eventually decouple Riot from pure crypto dependency.

- Profitability Pathway: Despite high revenue growth, when Riot becomes profitable remains unclear.

So, is Riot Platforms a moonshot or a minefield?

It’s both — and that’s what makes it one of the most watched tech-adjacent Bitcoin mining stocks in the U.S. right now.

for more news follow www.DailyGlobalDiary.com

Business

What’s Still Open on Christmas Eve 2025? The Stores, Restaurants and Major Chains Americans Are Rushing To

From last-minute groceries to fast food fixes and gift shopping, here’s who’s open on December 24 — and who’s closing early

Christmas Eve has quietly become one of America’s busiest shopping and dining days. As millions prepare for December 25 celebrations, another holiday ritual unfolds — the last-minute dash for groceries, gifts, prescriptions, or a quick bite before stores shutter early.

In 2025, most major retailers, grocery chains, and restaurants are open on Christmas Eve, though many are operating on reduced or special hours. Planning ahead matters, especially as closing times vary widely by location.

Here’s a clear, category-by-category breakdown of what’s open on December 24, 2025, across the U.S.

Grocery Stores Open on Christmas Eve 2025

If you’re missing ingredients for dinner or dessert, these grocery chains are welcoming customers — but not all day.

- Aldi — Open, most locations closing around 4 p.m.

- Food Lion — Open until 7 p.m.; pharmacies from 9 a.m. to 3 p.m.

- Stop & Shop — Open until 6 p.m.

- Trader Joe’s — Open, closing at 5 p.m.

- Wegmans — Closing at 6 p.m.

- Whole Foods — Regular opening, closing at 7 p.m.

Tip: Many stores stop restocking shelves hours before closing — earlier visits are safer.

Drugstores Open on Christmas Eve

Pharmacies remain essential stops for holiday travelers and families.

- CVS Pharmacy — Open, though hours vary by location

- Walgreens — Open; pharmacy hours may differ from retail hours

Fast-Food Chains & Restaurants Open on Christmas Eve

Hungry during the holiday scramble? You have options.

- Applebee’s — Select locations open

- Chick‑fil‑A — Open Christmas Eve (closed Dec 25)

- Burger King — Open at most locations

- Dunkin’ — Open, hours vary

- IHOP — Open

- McDonald’s — Open, location-based hours

- Taco Bell — Open

- Starbucks — Many stores open, reduced hours

Domino’s stores are not required to open — customers should check local listings.

Mail, USPS, UPS: Are Deliveries Running?

Yes — with exceptions.

- United States Postal Service locations are open

- Mail delivery runs except Priority Mail Express

- Blue collection boxes will be picked up December 24

- UPS will deliver packages, though pickup schedules vary

Last-Minute Gift Shopping: Retailers Open on Christmas Eve

Most major retailers are open — but many close early.

- Best Buy — 8 a.m. to 7 p.m.

- Costco — Open

- Dollar General — Many open until 10 p.m.

- Home Depot — Closing at 5 p.m.

- HomeGoods, Marshalls, T.J. Maxx, Sierra — 7 a.m. to 6 p.m.

- IKEA — Closing early (varies by location)

- JCPenney — Opens 9 a.m., closing varies

- Kohl’s — 7 a.m. to 7 p.m.

- Macy’s — 8 a.m. to 7 p.m.

- Michaels — 7 a.m. to 6 p.m.

- Petco — Most close at 7 p.m.

- Target — 7 a.m. to 8 p.m.

- Walmart — 6 a.m. to 6 p.m.

Is the Stock Market Open on Christmas Eve?

Yes — but only for a short session.

U.S. stock markets are open on December 24, closing early at 1 p.m. ET, instead of the usual 4 p.m.

The Bottom Line

Christmas Eve 2025 remains one of the most active retail days of the year — but timing is everything. Many stores close earlier than usual, and some services scale back well before evening.

If you’re heading out on December 24, check local hours first, plan efficiently, and don’t wait until nightfall — the doors may already be locked.

For more Update- DAILY GLOBAL DIARY

Business

Netflix Chiefs Walk the Warner Bros. Lot… A Power Move After Paramount Skydance’s Bid Is Rejected

As Warner Bros. Discovery shuts the door on Paramount Skydance, David Zaslav rolls out the red carpet for Netflix’s Ted Sarandos and Greg Peters

In Hollywood, timing is rarely accidental — and neither are photo ops.

On the very same day that Warner Bros. Discovery’s board officially rejected Paramount Skydance’s hostile bid, WBD CEO David Zaslav made a conspicuously public statement about where his company’s future may be headed.

Zaslav welcomed Netflix co-CEOs Ted Sarandos and Greg Peters to the iconic Warner Bros. Studio lot in Burbank — a visit documented through a series of carefully released images that quickly caught the industry’s attention.

The message was subtle in tone but loud in implication.

A Walk Through Hollywood History

Photos released by WBD on Wednesday show Zaslav strolling alongside Sarandos and Peters across the legendary studio grounds, including a stop in front of the instantly recognizable Warner Bros. Water Tower — a symbol of nearly a century of film and television history.

Officially, the visit was described as a meeting between Netflix leadership and executives at the studio. Unofficially, it read as a public endorsement of Netflix’s vision — and perhaps, its wallet.

ALSO READ : Taylor Swift Quietly Changes Lyrics to Two Reputation Songs on Apple Music, Swifties Go Into Detective Mode

Just weeks earlier, on December 5, Netflix had its $82.7 billion bid for WBD’s streaming and studios division accepted. That division includes crown-jewel assets such as Warner Bros. Pictures, HBO, HBO Max, and DC Studios.

Why the Paramount Skydance Bid Fell Flat

Earlier that same day, WBD’s board formally rejected the hostile takeover attempt from Paramount Global and Skydance Media — a move that insiders say reflected both strategic concerns and cultural misalignment.

While Paramount Skydance’s offer aimed to consolidate legacy media power, Netflix’s proposal centers squarely on streaming dominance, global scale, and technology-driven growth — areas where the streamer has already proven its reach.

By opening the gates of the Warner Bros. lot to Netflix’s top brass, Zaslav appeared to signal not just preference, but confidence in where the deal is heading.

A Not-So-Quiet Signal to Hollywood

Hollywood executives are well aware that studio tours are rarely casual affairs. Allowing Sarandos and Peters to be photographed on the lot — especially amid active acquisition talks — sends a clear signal to investors, talent, and competitors alike.

It suggests continuity rather than disruption. Legacy rather than liquidation.

Netflix, long viewed as the industry disruptor, has increasingly positioned itself as a studio caretaker, not just a streaming platform. The Warner Bros. assets would give Netflix unprecedented access to intellectual property, prestige brands, and theatrical infrastructure.

For Zaslav, the optics matter. In an industry still grappling with streaming losses, debt pressure, and shifting audience habits, stability — or at least the appearance of it — can be as valuable as the deal itself.

What Happens Next

While regulatory approvals and shareholder reactions still loom, the visit underscores a reality that few in Hollywood now ignore: the battle for the future of legacy studios is being fought not behind closed doors, but in plain sight.

And sometimes, a walk past a water tower says more than a press release ever could.

Business

From DVSA to AI fleets… key leadership moves reshaping transport, automotive and tech sectors this week

New appointments at DVSA, Aion Auto, Microlise, Leasing Options, Motive, and GRS Fleet Graphics signal a busy end to 2025 for industry leadership

It has been a decisive week for leadership across the UK’s transport, automotive, logistics and AI technology sectors, with a series of high-profile appointments aimed at tackling long-standing challenges and preparing businesses for rapid growth in 2026.

From clearing driving test backlogs to launching new car brands and scaling AI-powered fleet platforms, these moves underline how talent and experience are becoming central to operational reform.

New DVSA chief tasked with tackling driving test backlog

The Driver and Vehicle Standards Agency (DVSA) has confirmed Beverley Warmington as its new Chief Executive, effective January 5, 2026. She takes over from Loveday Ryder, who has led the agency since 2021.

Warmington arrives at a critical moment, with learner drivers across the UK facing prolonged test waiting times that have affected employment and mobility. She brings nearly 20 years of public service experience, most recently as Area Director for London, Essex and Eastern England at the Department for Work and Pensions (DWP), where she oversaw operations involving more than 12,000 staff.

UK Roads and Buses Minister Simon Lightwood praised the appointment, saying Warmington has the operational leadership needed to “grip the driving test backlog” and ensure reforms translate into faster, safer access to driving tests.

Aion Auto strengthens UK launch plans with senior marketing hire

As Aion Auto gears up for its UK market entry in 2026, the brand has appointed Alex Key as Marketing Director, reporting directly to Managing Director Jon Wakefield.

Key brings more than two decades of automotive marketing experience, having previously held senior roles at Honda, BMW Group, MINI, and Suzuki GB. Her recent work included helping steer Suzuki through a major rebrand and its first electric vehicle launch.

Wakefield said her ability to shape brand identity will be “pivotal” as Aion prepares to introduce itself to UK consumers in an increasingly competitive EV market.

Microlise appoints new CTO to drive logistics innovation

Transport technology specialist Microlise has named Dean Garvey-North as its new Chief Technology Officer, succeeding Duncan McCreadie, who retires after a decade with the company.

Garvey-North brings senior digital leadership experience from the utilities sector and management consultancy. He is also a member of Gartner’s CIO community and a contributor to the Forbes CIO Technology Council.

Microlise CEO Nadeem Raza said the appointment reinforces the company’s ambition to remain the UK’s most trusted name in transport technology, particularly as logistics firms push for efficiency, sustainability and smarter data-driven operations.

Leasing Options promotes Danielle Jones to head of marketing

Manchester-based vehicle leasing firm Leasing Options has promoted Danielle Jones to Head of Marketing, recognising her role in a major transformation of the brand’s digital and customer strategy.

Since joining in 2024, Jones has led a rebrand, rolled out new TV and audio campaigns, and overhauled email marketing with redesigned customer journeys. In her expanded role, she will oversee all marketing, lead generation, social media and PR activity.

Chief Operating Officer Mike Thompson described the promotion as a “natural next step” aligned with the company’s long-term growth ambitions.

Motive adds AI heavyweight to board

AI-powered operations platform Motive has appointed Adeyemi Ajao to its Board of Directors, strengthening its leadership as it scales internationally.

Ajao is the co-founder and managing partner of Base10 Partners, a venture capital firm focused on technology transforming the real economy. Motive CEO Shoaib Makani said Ajao’s experience as a founder and investor will help translate AI innovation into durable enterprise value.

GRS Fleet Graphics appoints operating partner to support growth

GRS Fleet Graphics has appointed James Hopkins as Operating Partner, a move designed to strengthen operational capability across both GRS and Epic Media Group.

Hopkins brings extensive experience across automotive operations, fleet management, telematics and B2B services. General Manager Martin Tyrrell said his leadership will be key as the business continues to scale and serve mid-size and large fleets across public and private sectors.

A clear trend heading into 2026

Taken together, these appointments point to a wider trend: organisations across transport, automotive and logistics are investing heavily in experienced leadership to modernise services, deploy AI, and improve customer outcomes.

As 2026 approaches, these executives will be under close watch — not just for strategy, but for execution.

For more Update – DAILY GLOBAL DIARY

“He-Man Wears a Suit…”: Why Nicholas Galitzine’s Masters of the Universe Trailer Has Fans Talking

Camilla Läckberg Isn’t Done Yet… The Queen of Swedish Noir Eyes Film, TV and a Bold Plan to ‘Conquer America’

“Screaming, Crying, Almost Throwing Up”… Sundance Insiders Reveal the Untold Chaos Behind America’s Most Influential Film Festival

From Swedish Noir to Hollywood Dreams Camilla Läckberg Has a Bigger Plan in Motion

When Sundance Nearly Fell Apart Insiders Recall the Chaos Behind the World’s Most Influential Film Festival

1-Iran Issues Dire Warning to Israel and Defies Trump on Nukes: “We’re Ready to Strike Deep Inside”

Donald Trump’s net worth reveals the fortune behind the former US President and business mogul

Caitlin Clark Sidelined with Quad Strain, Set to Miss Two Weeks of WNBA Action

Elon Musk Breaks Ranks with Trump Over ‘Big, Beautiful’ Tax Bill

“Tomás Rodríguez Net Worth 2025: Panama’s Gold Cup Goal‑Machine’s Surprising Fortune Revealed”

Miss Jamaica Suffers Terrifying Fall Off Miss Universe Stage; Rushed to Hospital on Stretcher in Viral Video

Moana Live-Action Teaser Sparks Outrage as Fans Call Disney’s Move a ‘Clear Money Grab’ — What Went Wrong?

Ryan Gosling’s Project Hail Mary Trailer Stuns Fans with a Mysterious Alien Ally and a Mission That Could Save Earth

Apple delays Jessica Chastain thriller The Savant about domestic extremism after recent US violence

Avatar 3, Fire and Ash trailer reveals Jake Sully’s family facing terrifying new Na’vi enemies with deadly fire powers

-

Entertainment1 week ago

Entertainment1 week agoHe-Man Wears a Suit Now… Nicholas Galitzine’s ‘Masters of the Universe’ Trailer Drops a Shock Fans Didn’t See Coming

-

Entertainment1 week ago

Entertainment1 week agoBrazil Eyes Oscar History Again… ‘The Secret Agent’ Scores Best Picture Nomination as Wagner Moura Stuns Hollywood

-

Entertainment5 days ago

Entertainment5 days ago“Comedy Needs Courage Again…”: Judd Apatow Opens Up on Mel Brooks, Talking to Rob Reiner, and Why Studio Laughs Have Vanished

-

Entertainment1 week ago

Entertainment1 week agoOscars Go Global in a Big Way as This Year’s Nominations Signal a New Era: ‘The Academy Is Finally Looking Beyond Hollywood…’

-

Entertainment1 week ago

Entertainment1 week ago“Dangerously Kinky… and Darkly Funny”: Olivia Wilde and Cooper Hoffman Push Boundaries in ‘I Want Your Sex’

-

Sports1 week ago

Sports1 week agoA Strong Night for Caleb Williams Ends With Doubts About the Bears’ Late Decisions

-

Crime5 days ago

Crime5 days agoMan Accused in Tupac Shakur Killing Asks Judge to Exclude Critical Evidence

-

Politics1 week ago

Politics1 week agoWhy Bari Weiss Says Pulling a ‘60 Minutes’ Story Was the Right Call — Even If It Looked Radical